American Airlines is not in bankruptcy. It is not publicly saying it is preparing for bankruptcy. It is still one of the largest airlines in the world, with major hubs, a valuable loyalty program, extensive international partnerships and billions of dollars in available liquidity.

But if jet fuel prices remain elevated, American may face a harder financial test than Delta Air Lines and United Airlines because it has thinner margins, a heavier debt burden and less room to absorb sudden cost increases.

That does not mean American is on the edge of collapse. It means the airline could be forced into difficult choices faster than its two legacy rivals.

Fuel Is the Pressure Point

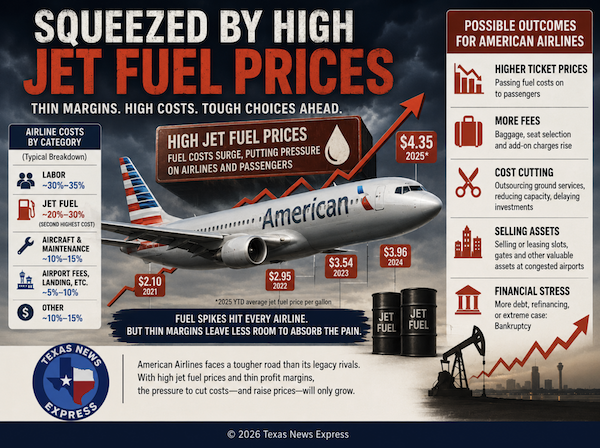

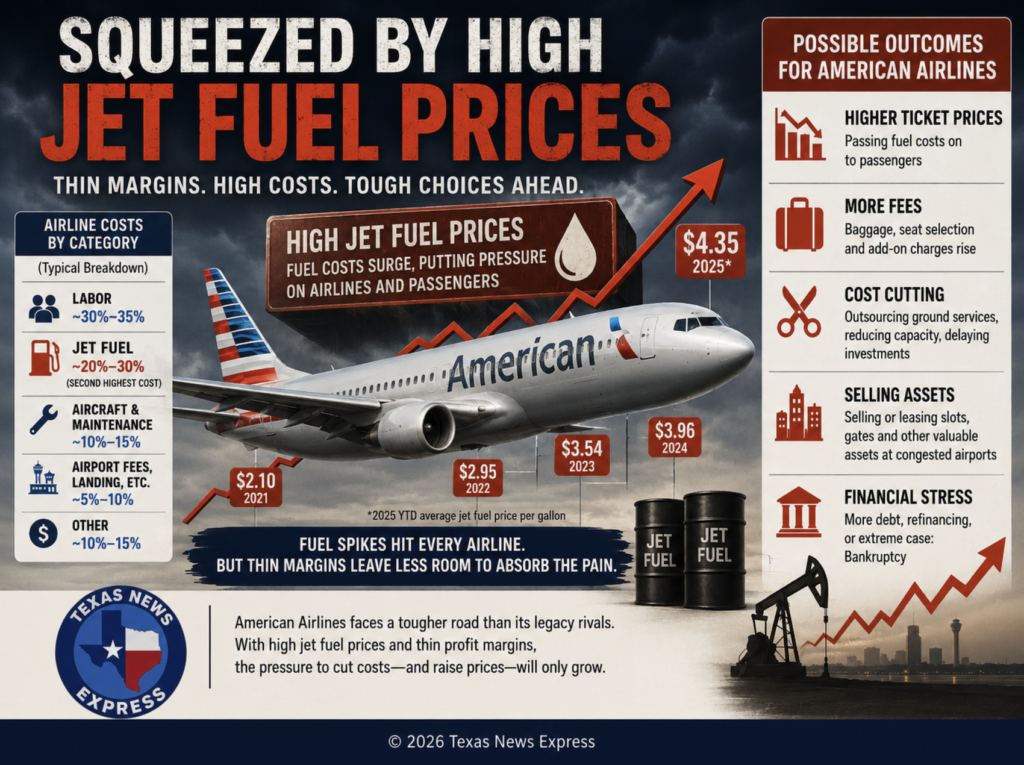

Jet fuel is usually the second-largest airline expense after labor, and that matters because fuel prices can move quickly while airline tickets are often sold weeks or months in advance. When fuel spikes after tickets have already been sold, airlines cannot immediately recover the full cost from passengers. AP reported that fuel is typically the second-biggest airline expense after labor, while the average jet fuel price at major U.S. hubs recently reached $4.88 per gallon, up from $2.50 before the latest Middle East conflict began.

That kind of jump can squeeze every carrier. But it does not squeeze every carrier equally.

Reuters reported that fuel accounts for roughly a quarter of airline operating costs and that low-cost and ultra-low-cost carriers are especially vulnerable when fuel stays high. The same report said Delta and United are better positioned than peers because of stronger margins, liquidity and premium revenue, while American faces pressure from its debt load and thinner financial cushion.

American Has Revenue, But Not Much Cushion

American reported record first-quarter 2026 revenue of $13.9 billion, but it also posted a GAAP net loss of $382 million, or $267 million excluding special items. The company ended the quarter with $34.7 billion in total debt, which American said was its lowest total debt level since mid-2015.

That is the central contradiction in American’s position: the company can generate enormous revenue, but its profit cushion is much thinner than Delta’s or United’s.

For full-year 2025, American reported record revenue of $54.6 billion, but only $111 million in GAAP net income and $237 million excluding special items. By comparison, Delta reported 2025 operating income of $5.8 billion, a 9.2% GAAP operating margin, $6.2 billion in pre-tax income and year-end debt and finance lease obligations of $14.1 billion.

That gap matters. When fuel rises, a company with a 9% or 10% operating margin has more room to absorb a shock. A company earning very little profit on more than $50 billion in annual revenue has much less room.

Delta and United Can Share the Pain. Can American?

Delta and United have already shown how stronger airlines respond to fuel shocks: absorb part of the cost, pass part of it to passengers and use premium revenue to protect margins.

Reuters reported that Delta and Southwest raised checked-bag fees by $10 as jet fuel prices surged, bringing first-bag fees to $45 and second-bag fees to $55 on affected routes. The same report noted that Delta has an additional buffer through its Pennsylvania refinery, which supplies a large share of its fuel needs, though Delta is still exposed to crude oil price spikes.

United also raised checked-bag fees to $45 for a first bag and $55 for a second bag on many routes, and AP reported that United CEO Scott Kirby said rising fuel costs had already added roughly $400 million to operating costs. United’s own first-quarter results said the airline absorbed a $340 million increase in fuel expense compared with the first quarter of 2025, while premium revenue rose 14%, loyalty revenue rose 13% and business revenue rose 14%.

That is the advantage Delta and United have: they can lean on premium cabins, business travelers, loyalty programs and stronger margins.

American can raise prices too. It can increase fares, bag fees and other charges. But the key question is whether it has enough room to absorb the portion of fuel increases that cannot immediately be passed to customers.

Reuters reported that American expected to end the March quarter with more than $10 billion in available liquidity, but also carried about $25 billion in long-term debt. Reuters also reported that every 1-cent increase in jet fuel prices adds about $50 million to American’s annual costs, and that CEO Robert Isom said the fuel run-up had added about $400 million to first-quarter costs.

That math is difficult. If American cannot recover fuel costs quickly enough through higher fares and fees, its already thin margins could disappear.

What Financial Trouble Could Look Like

The most likely first step would not be bankruptcy. It would be defensive management.

American could raise ticket prices, increase baggage fees, tighten award availability, reduce fare sales and push more customers toward paid upgrades. It could also trim flights that are full but not profitable once fuel is included. A route can look successful on passenger numbers and still be weak financially if fuel, labor and airport costs are too high.

The next stage could be cost cutting. American could reduce capacity in weaker markets, delay aircraft spending, slow hiring, park older or less fuel-efficient aircraft, and outsource more ground-handling work at smaller outstations to third-party ground-service companies. That type of outsourcing would be controversial with labor groups, but it is one of the more obvious ways airlines try to reduce fixed costs outside major hubs.

Another possible pressure valve would be asset sales. American could sell or lease valuable airport assets, gates or slots at congested, high-demand airports. Slots at airports such as New York LaGuardia, JFK, Washington Reagan National or other constrained markets can be extremely valuable because they control access to limited-capacity airports. Selling or leasing them could raise cash, but it could also weaken American’s long-term competitive position.

A more severe scenario would involve refinancing, new borrowing, sale-leaseback transactions, or asking vendors and aircraft lessors for concessions. These are not bankruptcy, but they are signs of a company trying to preserve liquidity.

Bankruptcy would be the extreme case. It would likely require more than high fuel prices alone. It would probably involve a combination of prolonged fuel inflation, weak demand, an economic slowdown, heavy debt-service pressure, labor cost pressure and limited ability to raise fares. In that scenario, bankruptcy could allow American to restructure debt, renegotiate contracts and shed obligations. But that is not the current base case based on the public information available.

Why Low-Cost Carriers May Feel It First

American’s problem is serious, but ultra-low-cost and low-cost carriers may feel the fuel shock even faster.

Spirit, Frontier and JetBlue operate with different business models than the legacy carriers. They rely heavily on price-sensitive travelers, lower fares and high aircraft utilization. When fuel rises sharply, they often have less room to raise fares without losing customers. Reuters reported that Moody’s viewed low-cost and ultra-low-cost carriers as especially exposed because JetBlue, Spirit and Frontier were already unprofitable last year before the latest fuel spike.

That helps explain why Delta and United may see opportunity in a fuel crisis. Stronger airlines can keep investing while weaker airlines cut routes, park aircraft or raise cash. United’s CEO even described the possibility of buying assets or absorbing network changes if rivals stumble, according to Reuters.

American sits somewhere in the middle. It is not as exposed as a distressed ultra-low-cost carrier, but it also does not have Delta’s margins or United’s momentum.

The Passenger Impact

For passengers, the likely result is higher total travel costs.

Base fares may rise. Checked-bag fees may rise. Seat-selection fees, premium-cabin fare tiers and change-related charges may become more important revenue tools. Airlines may also reduce capacity on routes where passengers are unwilling to pay enough to cover higher costs.

That means travelers could see fewer cheap fares, fewer nonstop options in smaller markets and more add-on fees. The pain may be especially noticeable in cities where American has marginal routes that depend on strong demand and manageable fuel costs.

American’s Real Problem Is Not Fuel Alone

Fuel is the trigger, but American’s deeper challenge is structural.

The airline has scale, brand recognition and a massive network. But compared with Delta and United, American has had weaker margins, more debt pressure and less financial room for error. When fuel prices are stable, that difference is manageable. When fuel prices spike, it becomes dangerous.

American can survive high fuel prices if demand stays strong, fares rise, premium revenue improves and management keeps cutting debt. But if fuel remains elevated and passengers resist higher prices, American may have to make choices that are painful for employees, customers and smaller communities.

Bankruptcy is not the most likely immediate outcome. But higher fares, more fees, outsourcing, route cuts, deferred investments and possible asset sales are all realistic pressure points if fuel prices stay high.

The question is not whether American Airlines can keep flying. It almost certainly can.

The question is how much of the airline it can protect if fuel prices stay high and its thinner margins leave little room to absorb the shock.